The machinery sector in Brazil is being severely impacted by an economic downturn (Brazilian GDP is expected to contract 1.5% in 2015).

- Deterioration across all main subsectors

- Many businesses are highly geared

- Increasing payment delays and insolvencies

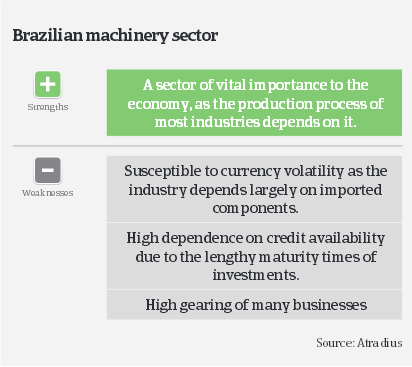

Machinery and equipment production is one of Brazil’s major industrial sectors, accounting for approximately 7% of the country’s overall Industrial production. Currently the sector is being severely impacted by an economic downturn (Brazilian GDP is expected to contract 1.5% in 2015). The whole Brazilian business environment has deteriorated due to decreased export revenues from commodities, decreasing industrial production and rising inflation (more than 8% in the first half of 2015), growing unemployment and exchange rate volatility.

The machinery sector mainly suffers from a decrease in investments, triggered by high interest rates and the current crisis in the oil/gas sector, which is a major buyer industry (the oil/gas industry is affected by lower oil prices and a large corruption scandal involving the state-owned Petrobras energy company). Additionally, there are cuts in government investment programs due to austerity measures, and the commodity export boom has ended for the time being. The high volatility of the Brazilian Real against the USD has also negatively affected the machinery business. The central bank needs to keep the general level of prices under control in order to avoid further deterioration of consumers´ purchasing power and has currently only limited options to use its reserves in the secondary market to stabilize the exchange rate (as it did in the past).

The agricultural machinery subsector is affected by falling commodity prices (mainly for soybeans and corn), which has resulted in lower margins for farmers, leading to lower investment. The prospects for the 2015/16 season suggest farmers´ margins will decrease further.

Oil and gas machinery equipment has been affected by lower investment of the energy sector, as the lower oil price has a very negative impact on this industry – given the high costs for exploration of Brazils´ pre-salt oil fields. Additionally machinery sales have been hit by a major corruption scandal involving the stat eowned energy company Petrobras and suppliers, as investments came to halt. At the same time road equipment machinery is hit by government austerity.

Therefore, in all machinery segments both demand and profit margins have significantly deteriorated over the last 12 months, and this negative trend is expected to continue in the second half of 2015.

Many machine businesses are highly indebted, due to large investments made in previous years when businesses expanded. Now that Brazil´s commodity-driven growth phase has ended for the time being, serving those debts has become increasingly difficult, mainly due to higher interest rates (the Brazilian central bank has repeatedly raised interest rates to combat inflation, and in June 2015 the benchmark interest rate was up to 13.75%).

This monetary policy has had a credit crunch effect, and it comes as no surprise that financial institutions´ willingness to provide loans to businesses remains very limited for the time being. The average payment duration in the Brazilian machinery industry

is 60-90 days, although there are exceptions when a buyer´s sector economic cycle tends to be longer (e.g. in agricultural machinery). Payment behaviour in the machinery sector is rather bad, as non-payments have increased in the first half of 2015 and are expected to increase further in the coming six months. Due to the credit crunch generated by high interest rates many businesses are stretching their payment terms. Insolvencies of machinery businesses´ have also increased, and a further rise in business failures is expected in the coming months.

Due to increasing credit insurance claims, the deteriorated business performance and increased credit risk, our underwriting stance is currently restrictive for all machinery subsectors. We are especially cautious with businesses that show weak financials, especially those which are highly geared and will most likely have problems serving their debts. Due to increased exchange rate volatility we also closely monitor businesses that are highly dependent on imported goods or semi-finished goods.

Související dokumenty

1003KB PDF